Cutler Commentary

Market Commentary 2Q22

June 30, 2022

Market Commentary

Recession- we won’t know if we are there until we already are.

A recession is not “officially” determined by two straight quarters of negative Gross Domestic Product (GDP) readings, but that definition has been used for so long that is has become accepted as fact. And during a very rough second quarter for stocks, the debate about whether or not the United States was already experiencing two quarters of negative growth was moot- investors clearly thought a recession had already arrived.

If so, this is an odd recession. Employment is booming. Hotels and flights are full. Consumers are flush with cash, and looking to spend the money they couldn’t spend for the last several years. Why would an economy with very low unemployment, solid household balance sheets, and reasonable bank debt levels be on the possible brink of recession? We all know the answer (unless you haven’t filled up your gas tank this year): inflation.

Stocks largely weathered the inflation storm during the First Quarter. It was bonds that started the year historically negative, having to adjust to shifting expectations from the Federal Reserve (the Fed) which was catching up from their “too low for too long” policy mistake. In the Second Quarter, we learned that inflation cannot be so easily tamed as Consumer Price Index readings kept coming in higher. After all, the money supply (M2) had grown by over $6 trillion during the pandemic, a feat not easily undone. The Fed’s response? More rate hikes and the onset of quantitative tightening; the Fed has now increased the lending rate 6 times (from 0% to 1.5%) and is expected to raise that rate somewhere between 5 and even 10 more times by year end. This increasingly hawkish Fed led to a stock market sell-off and we officially entered a bear market (a 20% drop) for the S&P 500 on June 13th. The S&P index finished the quarter down over 16%, with the Value aspect down roughly 11.5% while Growth stocks saw losses of over 20%.

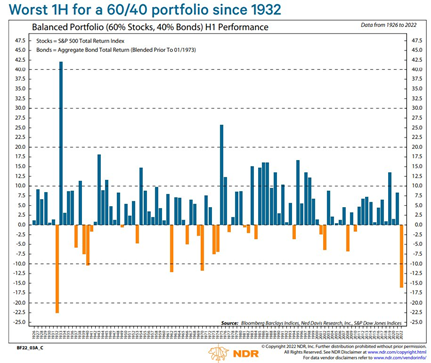

Bear markets are the “cost of admission” for equity investors. The risk that investors assume by owning stocks validates the returns that are achieved over long periods of time. Investors know that stocks carry risk. That does not make volatility any easier to stomach. But what has been especially troublesome for investors has been the simultaneous decline of historically uncorrelated assets classes. What does that mean? It means that both stocks and bonds have gone down together. That’s not supposed to happen! The nearby chart by Ned Davis Research shows just how bad this has been for diversified portfolios, with the worst returns for a standard “60% stock/40% bond” portfolio mix in nearly a century:

Bear markets are the “cost of admission” for equity investors. The risk that investors assume by owning stocks validates the returns that are achieved over long periods of time. Investors know that stocks carry risk. That does not make volatility any easier to stomach. But what has been especially troublesome for investors has been the simultaneous decline of historically uncorrelated assets classes. What does that mean? It means that both stocks and bonds have gone down together. That’s not supposed to happen! The nearby chart by Ned Davis Research shows just how bad this has been for diversified portfolios, with the worst returns for a standard “60% stock/40% bond” portfolio mix in nearly a century:

In the face of such nearly unprecedented bad news, we wanted to present some silver linings for investors to consider:

Silver lining #1: Is inflation peaking? Have you noticed lingering real estate listings in your neighborhood? Gas prices surged into June. But, oil recently dropped back under $100/barrel (after a high of $130 earlier in the year). We have witnessed significant drops across most commodities, notably lumber and copper. Even gold, the longstanding “inflation hedge” is down this year. Many retailers are overstocked and sitting on high inventories (as Target noted in their recent earnings call). We could see sizable markdowns as retailers look to offload overstocked items. It is possible we may see lower inflation even without peace in Ukraine. Rents are the fly in the ointment for inflation, as they continue to climb. But, what happens if inflation moderates? Our view is that stocks will move up as the Fed takes their foot off of the economy’s brakes.

Silver lining #2: Yields matter once again. When markets are speculative, cash flows don’t matter. Bitcoin goes to the moon, and SPACs/NFTs (pick your acronym) become the rage. As Warren Buffett said, “Only when the tide goes out do you discover who’s been swimming naked.” Well, the tide is out, and your portfolio is wearing cash flows. Dividend stocks are holding up well. Bond yields, especially after the drop we saw in the first half, are more attractive. The yield-curve, normally upward sloping, is effectively flat. This means investors see rates (and inflation) peaking as we enter a recession. What to do now? Find cash flows you are comfortable with to swim through the recession. In our view, that means dividends and high-quality shorter-term bonds, investments we have historically favored in client portfolios.

Silver lining #3: Stock valuations are back within historical norms. With interest rates near 0% for several years, there has been almost no price where stocks were not attractive versus bonds. TINA (There Is No Alternative) was the equity investor’s mantra. However, today rates are higher, and equities have fallen back into historically average valuation levels at roughly 16x earnings (source: JP Morgan). This means that they also should hold less risk today than at elevated valuations, a fact that should reassure market participants. The question now is, “Can companies weather a recession without too much of an impact on their earnings streams?” We are already seeing companies (such as Facebook, aka Meta) announce hiring slowdowns to control their costs. Without revenue growth, cost control will become the corporate tactic du jour. Revenues are difficult to increase in the face of a -1.6% Q1 Gross Domestic Product (GDP) growth, coupled with the current negative Q2 GDP projection (source: Atlanta Fed).

Looking forward, we expect volatility to remain elevated, especially as the word “recession” becomes more prevalent- whether we are officially in such a period or not. However, we believe that this is not a time to abandon stocks. The broad indexes are already sold down to a point where the market seems to expect a deeper, longer recession than what Cutler would expect. Why the optimism? In our view, we have never experienced a recession with such a well-capitalized economy. Inflation has been driven higher by monetary mistakes and supply-chain disruption, and these problems are both being dealt with aggressively. We continue to monitor the impact of a possible re-opening of China (Chinese stocks were actually 2.6% positive last quarter!*), which may impact both inflation and global growth. As we look forward to the third quarter, moving past the inevitable uncertainty that will arise during the US mid-term election cycle is also a potential catalyst.

Asset Class Review

The second quarter saw drops in every stock sector for the S&P, with losses ranging from 4.5% for the Energy sector to 25% for the Communications sector. Yes, even energy stocks were down this quarter! The broad S&P index finished the quarter down over 16%. The Value style of stocks clearly outpaced Growth for another quarter, but unfortunately no sector or style was immune from selling pressure.

Bonds also broadly saw losses in the period, though they were much lower than those in stocks. There was some flight to safety here as the 10-Year Treasury yield moved from a high mark of 3.4% down closer to 3.1% (bond prices going up means relative yield goes down). Even the 1-year Treasury managed to reach the 3% yield level during the quarter, which is remarkable after starting this year close to 0.5% effective yield. Looking forward, the trajectory of bond yields will be closely tied to actions by the Fed and changing expectations of expected increases. We believe bonds will continue to “decouple” from stock returns after moving together for large portions of this year to date, a development which could be welcome for conservative investors looking for portfolio stability. The Barclays Aggregate Bond index was down about 4.5% for the quarter, as traders grappled with how many times the Fed would further increase rates. The High Yield (aka Junk Bond) index had a very poor period, with that index down over 9% and credit spreads (the difference between Junk Bond yields and Treasury Bond yields) widening to their largest levels since early 2020. This is also a sign of investors anticipating further economic slowdown.

Alternatives allocations have shown capacity to provide value in this environment. Our preferred “alts” vehicle, the Goldman Sachs Absolute Return Tracker fund, was down for the period but is still well ahead of both broad stocks and bonds for the year to date. The ability to short some overvalued positions has helped this strategy in a bear market, as did positioning toward commodities- an investment class often associated with alternative investments. As mentioned earlier, commodities did not see the same outsized gains as the first quarter, but were still broadly positive in the second quarter. Oil futures rallied into June, though those prices did see some reduction as the quarter ended. Agricultural commodities saw a mixed quarter, as some concerns about lack of supply proved overdone but prices still increased on the possibility of specific shortages. As we progress into July, we have seen further weakness in commodities based on diminished growth expectations. Gold continued to show its lack of true inflationary hedging, as that metal was down 6% in 2Q. Some had considered Bitcoin as a possible inflation hedge, but the second quarter’s 60% drop has put that theory to bed.

Foreign developed stocks were not immune to the sell-off, but did have relative outperformance versus domestic stocks. Emerging markets stocks were also down, but had the best relative returns versus both domestic stocks and foreign developed stocks. The class was helped by China moderating their Zero Covid policy (for now) and some optimism about reopening, as well as their already lower valuation levels finding some bargain hunters. Global diversification continues to be an emphasis for Cutler, as valuations remain attractive and the dollar has had a multi-year strengthening. We continue to see upside potential and diversification benefits for investors in these asset classes.

Past performance is not indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment or strategy will be profitable or suitable for a particular investor's financial situation or risk tolerance. Investing involves risk, including loss of principal. You cannot invest directly in an index. Asset allocation and portfolio diversification cannot assure or guarantee better performance and cannot eliminate the risk of investment losses. Source: Morningstar

The S&P 500 Index is widely regarded as the best single gauge of large-cap U.S. equities. The index includes 500 leading companies and captures approximately 80% coverage of available market capitalization.

The Barclay's Aggregate Bond Index (Taxable Bond) is a broad base, market capitalization weighted bond market index

representing intermediate term investment grade bonds traded in the United States.

Headline Inflation is the raw inflation figure reported through the Consumer Price Index (CPI) that is released monthly by the Bureau of Labor Statistics.

The Bloomberg Commodity Index (Commodities) is an index of the prices of items such as wheat, corn, soybeans, coffee, sugar, cocoa, hogs, cotton, cattle, oil, natural gas, aluminum, copper, lead, nickel, zinc, gold and silver. The index is calculated on an excess return basis and reflects commodity futures price movements.

The MSCI EAFE Index (Foreign Developed Index) is designed to represent the performance of large and mid-cap securities across 21 developed markets, including countries in Europe, Australasia and the Far East, excluding the U.S. and Canada.

The MSCI Emerging Markets Index captures large and mid-cap representation across 27 Emerging Markets (EM) countries. With 1,392 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

Bitcoin Each crypto index is made up of a selection of cryptocurrencies, grouped together and weighted by market capitalization (market cap). The market cap of a cryptocurrency is calculated by multiplying the number of units of a specific coin by its current market value against the US dollar.

*Returns based upon the price return of FXI, the ishares Chinese Large-Cap ETF

All opinions and data included in this commentary are as of June 30, 2022 and are subject to change. The opinions and views expressed herein are of Cutler Investment Counsel, LLC and are not intended to be a forecast of future events, a guarantee of future results or investment advice. This report is provided for informational purposes only and should not be considered a recommendation or solicitation to purchase securities. This information should not be used as the sole basis to make any investment decision. The statistics have been obtained from sources believed to be reliable, but the accuracy and completeness of this information cannot be guaranteed. Neither Cutler Investment Counsel, LLC nor its information providers are responsible for any damages or losses arising from any use of this information.

CATEGORIES

Disclaimer

These blogs are provided for informational purposes only and represent Cutler Investment Group’s (“Cutler”) views as of the date of posting. Such views are subject to change at any point without notice. The information in the blogs should not be considered investment advice or a recommendation to buy or sell any types of securities. Some of the information provided has been obtained from third party sources believed to be reliable but such information is not guaranteed. Cutler has not taken into account the investment objectives, financial situation or particular needs of any individual investor. There is a risk of loss from an investment in securities, including the risk of loss of principal. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable or suitable for a particular investor's financial situation or risk tolerance. Any forward looking statements or forecasts are based on assumptions and actual results are expected to vary. No reliance should be placed on, and no guarantee should be assumed from, any such statements or forecasts when making any investment decision.